Looking for affordable new homes in Dallas-Fort Worth (DFW)? Here’s what you need to know:

- Affordable Range: New homes in DFW typically cost between $250,000 and $450,000, with a median price of $344,510 for a 3-bedroom home.

- Top Areas: Budget-friendly options are in suburbs like Forney, Princeton, and Crowley, while Midlothian offers lower taxes in many neighborhoods.

- Builder Incentives: Many builders offer perks like $10,000–$30,000 in rate buydowns or closing cost credits to lower upfront costs.

- Tax Considerations: Property taxes vary widely, often influenced by MUD/PID districts, which can significantly impact monthly payments.

- Key Tip: Always evaluate the total monthly costs (mortgage, taxes, insurance) instead of just the list price.

Working with relocation experts ensures you navigate builder contracts, negotiate incentives, and avoid common pitfalls. Whether you’re a first-time buyer or relocating, understanding the DFW market will help you make informed decisions.

The DFW New Construction Market at a Glance

Price Ranges and Home Types

The Dallas-Fort Worth (DFW) new construction market can be divided into three main price tiers. Entry-level homes, priced under $450,000, are geared toward first-time buyers. Move-up homes typically range from $550,000 to $900,000, while luxury properties begin at $1 million and can go far beyond that.

Entry-level homes in the region generally feature single-family detached designs, offering 3–5 bedrooms, 2–3 bathrooms, a 2-car garage, and between 1,200 and 1,800 square feet of living space. Open-concept floor plans are the norm, and many builders now include smart home technology and updated finishes as standard features rather than optional upgrades.

One potential surprise for buyers in DFW is the prevalence of special tax districts. Around 80–90% of new developments are located within a Municipal Utility District (MUD) or Public Improvement District (PID). These districts fund essential infrastructure like roads and utilities but can significantly impact property tax rates. In some communities, tax rates can exceed 3.0%, compared to less than 1.6% in others. These tax differences can heavily influence monthly payments, making it crucial for buyers to review sample tax bills before committing to a purchase. Understanding these tax implications is vital for navigating the market’s diverse offerings.

Affordable Submarkets Worth Knowing

As prices rise in established suburbs like Prosper, where homes often exceed $600,000–$800,000, affordability in DFW increasingly lies in outer communities where land is still reasonably priced. Below is a table showcasing some of the most budget-friendly submarkets:

| Area | Starting Price | What Makes It Stand Out |

|---|---|---|

| Princeton | From $234,990 | Strong price-per-square-foot value; A/B rated schools |

| Pilot Point | From $264,990 | Emerging affordable corridor north of Dallas |

| Forney | From $275,960 | Large lots and generous square footage for the price |

| Heartland | From $242,990 | Master-planned amenities at entry-level pricing |

| Midlothian | High $300s–$500s | Many neighborhoods are free from MUD/PID taxes |

| Anna | From $350,990 | Northern expansion with strong growth potential |

Local factors, such as MUD/PID taxes, further shape the appeal of these submarkets. For instance, Midlothian stands out for its strong schools and absence of MUD/PID taxes, making it a compelling choice compared to many eastern corridor communities. On the other hand, Forney offers excellent square footage for the price but often comes with MUD/PID taxes.

When buying in DFW, it’s not just about the list price. Two homes with identical sticker prices can have vastly different monthly payments once taxes, insurance, and financing incentives are factored in. Understanding both the pricing tiers and the tax landscape is essential to finding a new build that truly fits your budget.

sbb-itb-9bb2e84

Where to Find Affordable New Construction in DFW

What to Look for When Choosing an Area

Finding affordable new homes in the Dallas-Fort Worth area means weighing a mix of factors like price, property taxes, and school district quality. These three elements overlap to create the true cost of homeownership, and the sweet spot lies where they all align.

Property tax rates across DFW vary widely, from under 1.6% in places like Rockwall and Heath to over 3.0% in other areas. Generally, rates below 2.6%–2.7% are considered low, and this difference can significantly impact your monthly payment – sometimes by hundreds of dollars. While the sale price is important, tax rates play a major role in long-term affordability, even if they’re not obvious upfront.

School district ratings are another key factor, especially for resale value. Aim for districts rated B+ or higher, but double-check the specific school assigned to your potential lot. Fast-growing areas often see boundary changes, which can affect school assignments.

Daily commute and highway access also shape the livability of a home. For example, the US 380 corridor between Prosper and Princeton has seen a lot of builder activity, but traffic congestion can be a drawback. Balancing commute times with other priorities is crucial before settling on a location.

These considerations lead us to some of the most promising neighborhoods in the region, listed below.

Top Affordable Neighborhoods in DFW

Here are some neighborhoods that strike a balance between taxes, school quality, and price per square foot, catering to different buyer priorities:

| Area | Best For | Typical Price Range | Tax Notes |

|---|---|---|---|

| Kaufman County (Forney, Terrell) | Largest home/lot for the money | $400,000s+ | Generally lower overall |

| Princeton | Value in the north corridor | $400,000s+ | Often includes MUD/PID |

| Midlothian | Balanced taxes, schools, & size | High $300,000s–$500,000s | Many MUD/PID-free zones |

| Rockwall/Heath | Lowest tax rates in the region | High $400,000s+ | As low as ~1.5% |

| Crowley/Fort Worth suburbs | Entry-level affordability | Under $300,000–$400,000s | Strong local growth |

"If your primary goal is getting the biggest home or lot for the money and keeping property taxes relatively low, look to Kaufman County pockets – Forney, Terrell, and surrounding towns." – Zak Schmidt, The New Construction Agent

Midlothian is an often-overlooked gem, offering mid-range pricing, solid schools, and neighborhoods without extra MUD/PID taxes.

"Midlothian is a sleeper hit for buyers who want a balance of taxes, schools, and square footage." – Zak Schmidt, The New Construction Agent

For buyers with tighter budgets, neighborhoods in West Dallas, South Dallas, and Crowley still have new construction homes under $300,000. However, livability can vary significantly by street, so visiting in person and doing thorough research is critical.

Beyond picking the right area, knowing how to search effectively can help uncover hidden opportunities.

Using Tools and Local Know-How to Find Listings

While the MLS is a great place to start your search for new construction homes, it doesn’t show everything. Many builders hold "pocket" listings or have upcoming phases that aren’t yet publicly listed. Connecting with a local expert can give you access to these off-market opportunities.

For example, Tom’s Texas Realty offers access to off-market listings, which can provide up to three times more options than the MLS alone. This kind of early access is particularly helpful in competitive areas where homes sell quickly. Working with a knowledgeable local agent ensures you can match your ideal neighborhood criteria with the right available properties.

Additionally, checking county appraisal district records can help you identify whether a development includes MUD or PID assessments. These fees can vary significantly, even between neighborhoods in the same city, and they directly impact your overall costs.

Working with Builders on Affordable New Construction

Types of Builders and What They Offer

Choosing the right builder can help you avoid unexpected expenses and delays.

Production builders, such as D.R. Horton and Lennar, stick to a set of pre-designed floor plans and fixed option packages. This streamlined process keeps costs lower and construction timelines predictable, making them a go-to choice for affordable new homes in the Dallas-Fort Worth (DFW) area. On the other hand, private or regional builders like Highland Homes and David Weekley Homes often provide more personalized customer service and higher-quality finishes as standard. However, they tend to offer fewer financing incentives. Semi-custom builders allow for structural changes to floor plans, but this flexibility comes with a higher price tag and longer construction times.

| Builder Type | Best For | Trade-Off |

|---|---|---|

| Production Builders | Affordable pricing and quick builds | Limited customization |

| Private/Regional | Better service and finishes | Fewer financing perks |

| Semi-Custom | Greater customization options | Higher cost and extended timelines |

| Spec/Inventory | Faster move-in availability | No say in finishes or lot choice |

Spec homes, which are already under construction or fully completed, can be a great option if you’re looking to move quickly. Builders often prefer to sell these homes fast to avoid carrying costs, making them more open to negotiation compared to homes that are still in the planning stages.

Next, let’s explore how to research builders and secure the best deals.

How to Research Builders and Negotiate Incentives

Start by checking out reviews from verified homeowners on platforms like TrustBuilder. For example, LGI Homes has a 4.7/5 rating, Beazer Homes scores 4.6/5, and Highland Homes lands at 4.5/5. These ratings reflect real experiences, offering insights beyond polished marketing testimonials.

When touring model homes, ask which features are standard and which are considered upgrades. Builders like Bloomfield Homes often use an "all included" approach, including many upgrades in the base price. Others might advertise a lower base price but expect buyers to spend an additional $20,000–$40,000 at the design center. It’s also worth investigating whether the builder operates independently or as part of a larger company. For instance, Centex belongs to PulteGroup, and Trophy Signature Homes is under Green Brick Partners. These affiliations can hint at financial stability and consistent quality.

Builders frequently offer incentives, but it’s critical to understand the fine print. For example, in early 2026, Beazer Homes provided a four-year rate buydown starting at 1.99% in Year 1 and increasing to 4.99% by Year 4. Meanwhile, Highland Homes offered "Your Way" flex credits of up to $50,000 on select inventory homes. However, most incentives require using the builder’s preferred lender, which may come with an interest rate 0.125% to 0.375% higher than other lenders. Always calculate whether the incentive offsets the potentially higher loan costs.

"Builder incentives are a trade – and if you do not understand the trade, you can end up overpaying, buying in the wrong location, or locking into a deal structure that costs more than it saves." – Paragon Realty Advisors

Finally, bring your own agent on your first visit to a model home. Many DFW builders require a buyer’s agent to be present during the initial tour to recognize their commission. If you visit alone, you might lose the chance for independent representation.

Builder Contracts and Construction Timelines

Once you’ve compared your options, understanding the terms of builder contracts and managing construction timelines becomes essential.

Unlike standard TREC resale contracts, builder contracts are often skewed in the builder’s favor. Texas law (HB 2024) mandates minimum warranty coverage of 1 year for workmanship, 2 years for mechanical and electrical systems, and 6 years for major structural components. However, these warranties can vary. For instance, Highland Homes reduced its structural warranty from 10 years to 6 years starting January 1, 2026.

Construction timelines can also be unpredictable. Add 60–90 days to the builder’s estimate to account for potential delays caused by weather, labor shortages, or supply chain issues. Misjudging this timeline could leave you scrambling if you’ve already sold your current home or ended your lease.

"New does not mean flawless, and a builder warranty is not a substitute for a professional quality control process." – Paragon Realty Advisors

To ensure quality, schedule independent inspections during key construction phases – foundation, pre-drywall, and final stages. These inspections often catch issues that builder quality control teams or municipal inspectors might miss.

When budgeting at the design center, prioritize structural upgrades like covered patios, additional bathrooms, or higher ceilings. These are difficult and costly to modify after construction. On the other hand, cosmetic choices like light fixtures or cabinet hardware can be updated more easily and affordably after closing.

Financing Your New Construction Home in DFW

Setting a Realistic Budget

When planning your budget, make sure to include more than just the purchase price. Factor in four key components: your monthly payment (including taxes and insurance), cash needed at closing, the interest rate structure, and the tax assessment basis.

One thing to watch out for is property tax reassessments, which can increase your monthly payment 12–18 months after closing. At first, lenders often calculate escrow based on the land’s value, which is much lower than the completed home’s assessed value. To avoid surprises later, ask your lender to base the property tax escrow on 80–90% of the finished home’s value upfront.

Another cost to account for is MUD and PID assessments, which are common in new DFW developments. These fees often make up part of the annual tax bill, so include them in your debt-to-income (DTI) calculation to get an accurate picture of your monthly costs. Around 80–90% of new developments in the area include these assessments. Don’t forget rising homeowners insurance costs, either – for a $400,000–$450,000 home in DFW, expect to pay $2,000–$2,500 per year.

"Early estimates = guesses. Until your lender pulls documents and your contract is locked, the realistic monthly payment remains an estimate." – Zak Schmidt, Real Estate Agent

It’s also wise to set aside a 10–15% contingency reserve for unexpected expenses, like changes during the design process or other overages. With your budget in place, you can start comparing loan options to find the best fit.

Comparing Loan Options

Here’s a quick overview of some common new construction loan types and their features:

| Loan Type | Down Payment | PMI Required | Best For |

|---|---|---|---|

| Construction-to-Permanent | 20–25% (typical) | No (if 20%+ down) | Custom builds on owned land |

| VA Construction | 0% | No | Eligible veterans |

| FHA Construction | 3.5% | Yes | Low down payment or flexible credit needs |

| Conventional | 3–20% | Depends | Production homes with builder incentives |

A construction-to-permanent loan combines the construction phase and permanent mortgage into one closing. You lock in your rate upfront, and during construction, you make interest-only payments. On the other hand, a construction-only loan requires a second closing to refinance into a permanent mortgage, which adds costs and increases the risk of rate changes.

For veterans, VA construction loans are a strong option with $0 down and no PMI, saving $100–$300 per month compared to conventional loans. Just make sure your builder is VA-approved early in the process. If you’re looking for a low down payment option, FHA construction loans allow for as little as 3.5% down and accept credit scores as low as 580. However, they do require both upfront and annual mortgage insurance.

Before committing to the builder’s preferred lender, get quotes from 2–3 independent lenders. Even a small rate difference, like 0.25%, could cost you over $20,000 over the life of a 30-year loan, potentially canceling out any upfront incentives from the builder.

"A builder’s lender package can be a great deal. It can also be priced in a way that quietly cancels out the savings the builder is offering on the front end." – Maureen Cappallo, Broker/Founder, Momentus Real Estate Group

Choosing the right loan can make a big difference in keeping your new home affordable in DFW’s competitive market.

Ways to Lower Upfront Costs

One way to reduce upfront costs is by asking the builder for "flex cash." Instead of requesting a price reduction (which can impact neighborhood appraisals), ask the builder to contribute toward closing costs or a rate buydown. In DFW, entry-level homes (under $450,000) often come with $10,000–$30,000 in flex cash offers, while homes in the $550,000–$900,000 range may include $20,000–$50,000 or more.

Spec homes, which are already under construction or completed, provide the best negotiating leverage. Builders are eager to sell these homes to avoid carrying costs, especially near the end of a quarter or year.

"Spec homes are your best negotiation opportunity. Builders are highly motivated to move sitting inventory, especially approaching quarter-end or year-end." – Bobby Franklin, REALTOR®

VA and FHA loans can also lower the cash needed at closing. If you already own land for a custom build, the appraised value of the land can often count toward your down payment. After closing, remember to file for the Texas homestead exemption right away – it’s free and can lower your home’s taxable assessed value.

To save even more, focus your budget at the design center on structural upgrades, like covered patios or higher ceilings. Cosmetic features, such as backsplashes or lighting, can be added later at a lower cost than the builder’s markup.

Top 5 Places In The 400s to Live in Dallas-Fort Worth for Families

Step-by-Step: How to Buy an Affordable New Build in DFW

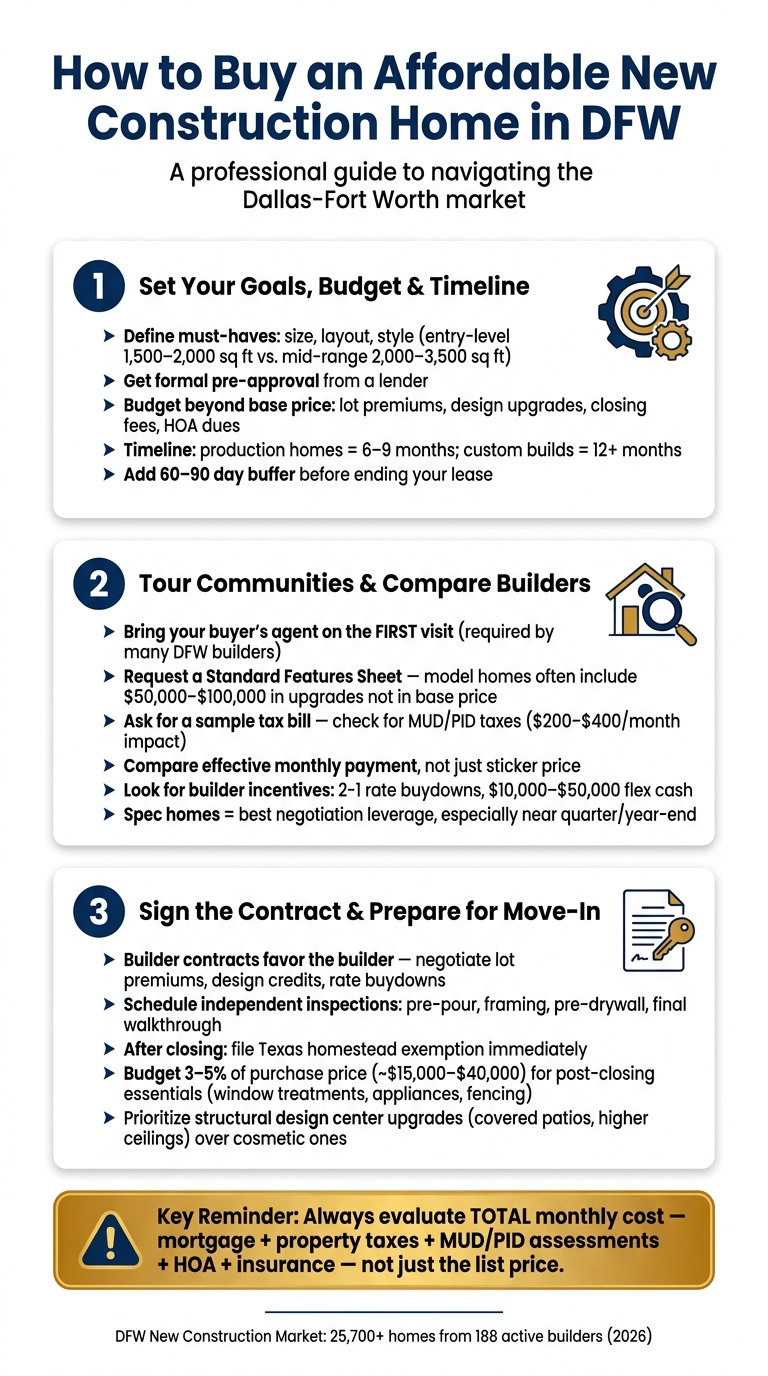

How to Buy an Affordable New Construction Home in DFW: Step-by-Step Guide

Step 1: Set Your Goals, Budget, and Timeline

Before you start touring homes, take time to outline your must-haves. Think about the size, layout, and style that fit your needs. Are you leaning toward a smaller, entry-level production home in the 1,500–2,000 sq. ft. range? Or do you need something bigger, like a mid-range home between 2,000–3,500 sq. ft.? These details will shape everything from your price range to the builders and neighborhoods you focus on.

Once you’ve nailed down your requirements, secure a formal pre-approval from a lender. This will give you a clear picture of your buying power before you start meeting with builders. Keep in mind that your budget should account for more than just the base price of the home. Factor in additional costs like lot premiums, design upgrades, closing fees, and HOA dues.

Time is another key consideration. Production homes typically take 6–9 months to complete, while custom builds can take a year or longer. If you’re renting, plan to include a 60–90 day buffer before giving notice on your lease to avoid timing issues.

With your goals and budget set, you’ll be ready to start comparing what different communities and builders have to offer.

Step 2: Tour Communities and Compare Builders

When visiting communities, make sure your buyer’s agent is with you from the start. Many builders in the DFW area require agents to be registered during your first visit. If you go alone, you might not be able to add an agent later, which means losing out on a knowledgeable advocate who can assist you at no extra cost.

During your tours, ask the sales representative for a Standard Features Sheet. This document is crucial because model homes often include $50,000–$100,000 worth of upgrades that aren’t reflected in the base price. Also, request a sample tax bill for the lot you’re considering, so you can evaluate any additional costs like MUD or PID taxes.

Don’t just focus on the base price of the home. Pay attention to the effective monthly payment, which can vary based on incentives. For example, a builder offering a 2-1 rate buydown or $20,000–$50,000 in flex cash might be a better overall deal than one with a lower sticker price but no incentives. Spec homes – those already under construction or completed – can also offer more room for negotiation, especially as builders approach the end of a fiscal quarter.

"The builder’s agent works for the builder, not for you. Their job is to sell the builder’s homes at the best possible price and terms – for the builder." – Paige Miranda, Miranda Realty Team

Step 3: Sign the Contract and Prepare for Move-In

Once you’ve compared your options and chosen a builder, it’s time to finalize the contract and start preparing for your move. Keep in mind that builder contracts in Texas are typically designed to favor the builder. For instance, they often don’t include penalties for construction delays and may offer limited warranties for workmanship. This is where your buyer’s agent becomes invaluable. They can help you review the contract and negotiate better terms. If the builder won’t budge on the base price, try negotiating for other benefits like reduced lot premiums, design center credits, or a permanent rate buydown.

After signing, schedule independent inspections at key construction phases: pre-pour (foundation), framing, pre-drywall, and the final walkthrough. While some builders might resist these inspections, they’re one of the best ways to protect your investment.

"The superintendent matters more than the builder’s brand – a great superintendent can deliver excellent outcomes with a mid-tier builder, while a poor superintendent can create nightmare experiences with premium builders." – Bobby Franklin, REALTOR®

Once you close on your new home, there are two immediate tasks to tackle. First, file your Texas homestead exemption with the county appraisal district. Second, set aside a budget for move-in essentials. Most new builds come as a "white box", meaning they lack items like window treatments, a refrigerator, washer/dryer, or backyard fencing. Expect to spend around 3–5% of the purchase price (roughly $15,000–$40,000) on these post-closing costs. For design center upgrades, prioritize structural changes – like covered patios, higher ceilings, or additional windows – since these are much harder and more expensive to add later.

Key Takeaways for Buying Affordable New Construction in DFW

Navigating the new construction market in Dallas-Fort Worth (DFW) requires a strategic approach. With over 25,700 homes available from 188 active builders as of early 2026, DFW ranks as the second-largest new construction market in the U.S.. But understanding the full financial picture is key to avoiding costly mistakes.

The most common pitfall? Focusing solely on the sticker price. Instead, buyers should evaluate the total monthly cost, which includes not just the mortgage but also property taxes, MUD/PID assessments (typically $200–$400 per month), HOA dues, and insurance.

Watch Out for the Tax Trap

One major challenge is the jump in escrow payments after the county reassesses your home. The first year’s escrow is based on the unimproved land value, but once your completed home is reassessed, payments can rise significantly in year two. To avoid this, consider requesting an upfront escrow based on 80–90% of your home’s finished value. Additionally, file your Texas homestead exemption immediately after closing to help manage property tax costs.

Builder Incentives: Proceed with Caution

Builders in 2026 are offering enticing incentives like flex cash, rate buydowns, and closing cost credits rather than reducing list prices. However, these perks can sometimes distract buyers from more critical factors like location, tax districts, and long-term costs. As Paragon Realty Advisors explains:

"Choosing new construction based on the shiniest incentive rather than the right location, tax district, and long-term cost structure is the most expensive mistake DFW buyers make."

This highlights the importance of thoroughly reviewing lender packages and understanding the true value of these offers.

The Value of Independent Representation

Having independent representation can lead to significant savings, often ranging from $15,000 to $30,000. Compare the builder’s preferred lender package with other options to ensure you’re getting the best deal. Partnering with a knowledgeable agent can also help with critical steps, such as:

- Decoding MUD/PID tax districts

- Reviewing builder contracts

- Coordinating independent inspections (pre-drywall, final walkthrough, and 11-month warranty stages)

For example, the team at Tom’s Texas Realty specializes in guiding buyers through these complexities, ensuring a smoother and more informed experience.

FAQs

How can I estimate my true monthly payment on a new build before I sign?

When calculating your actual monthly payment, it’s important to consider more than just the purchase price. Factor in property taxes, homeowners insurance, escrow payments, and any potential perks like builder incentives or rate buydowns. Keep in mind that property taxes may rise after your purchase, so it’s a good idea to ask your lender or real estate expert to estimate future costs. Taking all these elements into account will give you a clearer picture of your monthly financial commitment before you finalize the deal.

How do I find out if a community has MUD or PID taxes and what they’ll cost me?

To find out if a community has MUD (Municipal Utility District) or PID (Public Improvement District) taxes, start by asking the builder or sales representative for the total tax rate, including any special assessments. Then, double-check this information through official district or county records for accuracy. To get a clearer picture of the financial commitment, request an estimate of the monthly or annual assessments based on the property’s value. This helps you understand the long-term costs before making a purchase.

When do builder incentives stop being a good deal compared to a lower rate elsewhere?

When the total cost of a deal – including loan terms and long-term payments – outweighs the savings from builder incentives, those incentives lose their appeal. This can happen if the incentives are tied to reducing an interest rate that’s still higher than what you could find elsewhere or if accepting them means agreeing to less favorable loan terms overall.